Most people don't get in trouble because they buy something.

They get in trouble because they buy it while ignoring the hidden risk that comes with it.

... The payment that stretches the budget.

Risk is not always dramatic. It is usually quiet and delayed.

|

|

|

Risk Shows Up On Your Credit In Predictable Ways |

A purchase becomes a credit problem when it increases the chance you will miss payments or carry high balances.

Payment strain... new monthly payments reduce breathing room which increases late payment risk.

New credit temptation... financing offers can add hard inquiries and new accounts.

Snowball effect... one tight month turns into revolving balances and interest becomes the long term cost.

This is why risk is not just about the price tag. It is about whether the purchase increases the odds of negative credit behavior.

|

|

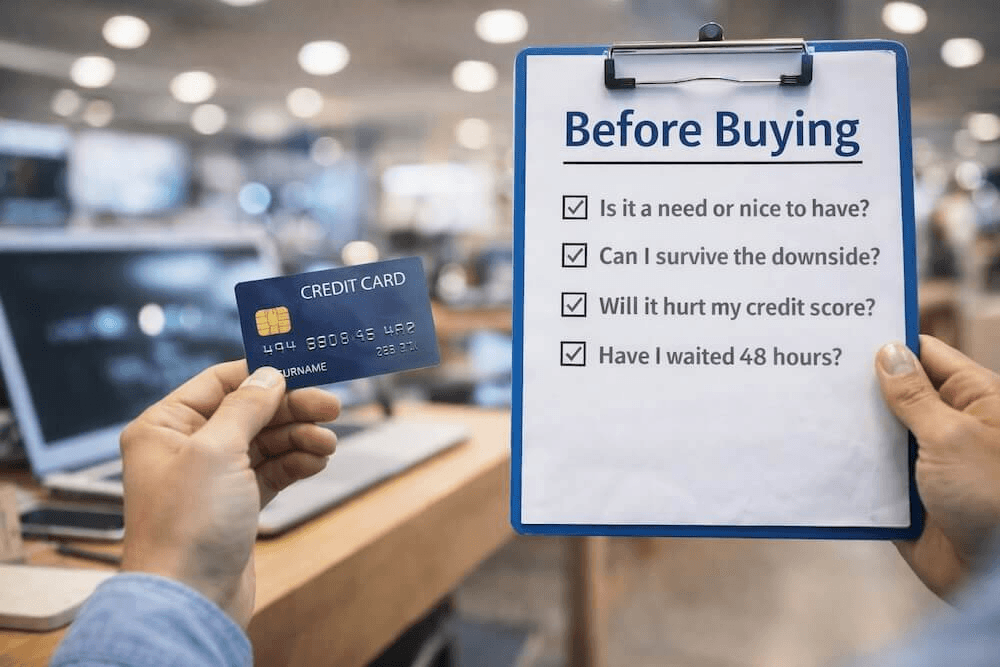

Use The 5 Minute Risk Filter Before Any Purchases |

Here is the filter. You can screenshot this...

Step 2: Price the downside

Step 3: Check your credit exposure

Step 4: Use the 48 hour rule for anything over your threshold

Step 5: Decide with one sentence

What is one purchase you are considering right now and which sentence fits it best? |

|

Anxiety is Data Not a Stop Sign |

|

|

Simple Tools That Prevent Regret |

The one page budget snapshot... income, fixed bills, minimum payments, food and gas, buffer.

Utilization guardrails... keep balances under 30 percent when possible and avoid crossing 50 percent if you are trying to rebuild fast.

Payment protection... autopay minimums on everything first then add extra payments manually.

|

Don't fear spending.

Just pause, price the downside and make a decision you can live with.

Before you buy it read this again:

If the downside is survivable and the purchase matches your plan it can be a yes.

Until next week,

Disclaimer: Guide to Perfect Credit and Credit Coach Rob provide financial education and coaching based on personal experience and research. We are not licensed financial advisors, accountants or attorneys. This content is for informational purposes only and should not be considered financial, legal or tax advice. Always consult with a certified professional for your specific situation. |

Get The 850 Pin! |

It’s more than a number... it’s a symbol of the journey. My journey started with free t-shirts and ended at 850.

What's yours? #850Journey #CreditComeback #YouGotThis |